- Apr 4, 2013

- 13,670

- 16,890

- AFL Club

- Fremantle

I'm not interested in your opinion. This is about a Treasurer contradicting himself on housing within the space of six months, and a government disagreeing with central bank and treasury officials who believe there are problems in certain sectors of the housing market. This is in addition to their financial system white paper which recommended resolving issues with negative gearing to fix problems in the housing market.No, that's MY considered opinion. I base it on the following...

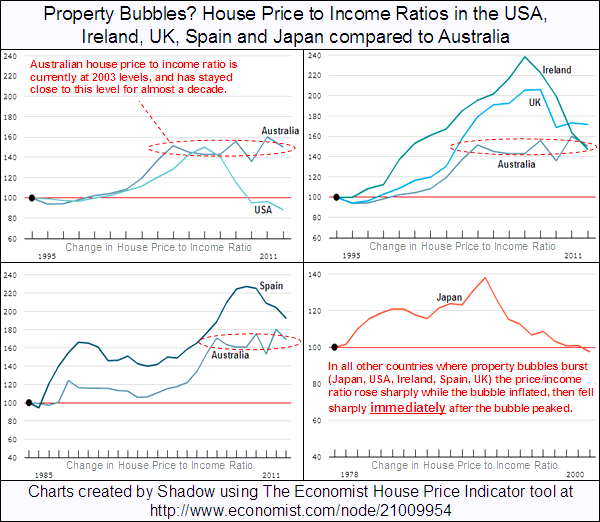

- Every other major property bubble hasn't looked like us, we've had a fairly consistent price to income ratio as our average incomes have increased a lot over the past decade.

- In Sydney less than 5% of home owners spend more than 30% of their income on their mortgage, so there is plenty of scope for interest rate increases to be absorbed, when they happen in the coming years. Our mortgage repossessions are as low as they've ever been in a few decades. Usually before a collapse, delinquency rates, mortgage repossession and loan impairment expenses start to creep up.

- We will have continued high population growth, our average rate of 1.8% recently is many times the OECD average. We're predicted to have a population of 10% more in 5 years, while that doesn't equate directly to 10% more homes, it equates to as many as we're building, so demand will continue to at worst match supply.

- Demand for property in Australia will continue to be higher than local fundamentals suggest, as we're seen as a stable investment compared to many of our neighbours.

What do you base your opinion we're in a property bubble on?

Every single government does well in a buoyant housing market, this government wants it to continue, despite other economic fundamentals being weak.