Gigantic

Brownlow Medallist

Look, they probably aren't wrong - but I wouldn't go bragging if I were a business surviving off moral hazard.

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

They aren't wrong but honestly that's really taking the piss.

Look, they probably aren't wrong - but I wouldn't go bragging if I were a business surviving off moral hazard.

Traditionally, crude is much more price sensitive to externalities than other bulk commodities.lol I don't know much but one thing I have learnt is pretty much nobody including the 'experts' ever has much of a clue in where oil prices ever goes.

After spending money toLook, they probably aren't wrong - but I wouldn't go bragging if I were a business surviving off moral hazard.

Where are the lithium bulls now?

The commodity price has dipped 40% since last November but Argonaut's David Franklyn isn't dumping ASX lithium stocks just yet.

a day ago

Print Wire

Glenn Freeman

Livewire Markets

Elon Musk, the founder of the world’s best-known electric vehicle maker Tesla (NASDAQ: TSLA), is now building his own town. That’s just one (slightly hare-brained) indicator of the demand for and profitability of EVs.

Lithium carbonate pricing is another, given that the metal is one of the core components of the lithium-ion batteries used in most EVs – nickel-hydride batteries are often used in hybrid vehicles.

Demand for EVs is ramping up strongly – as is the demand for lithium, which is also a key element in several other applications, including renewable energy production and storage batteries.

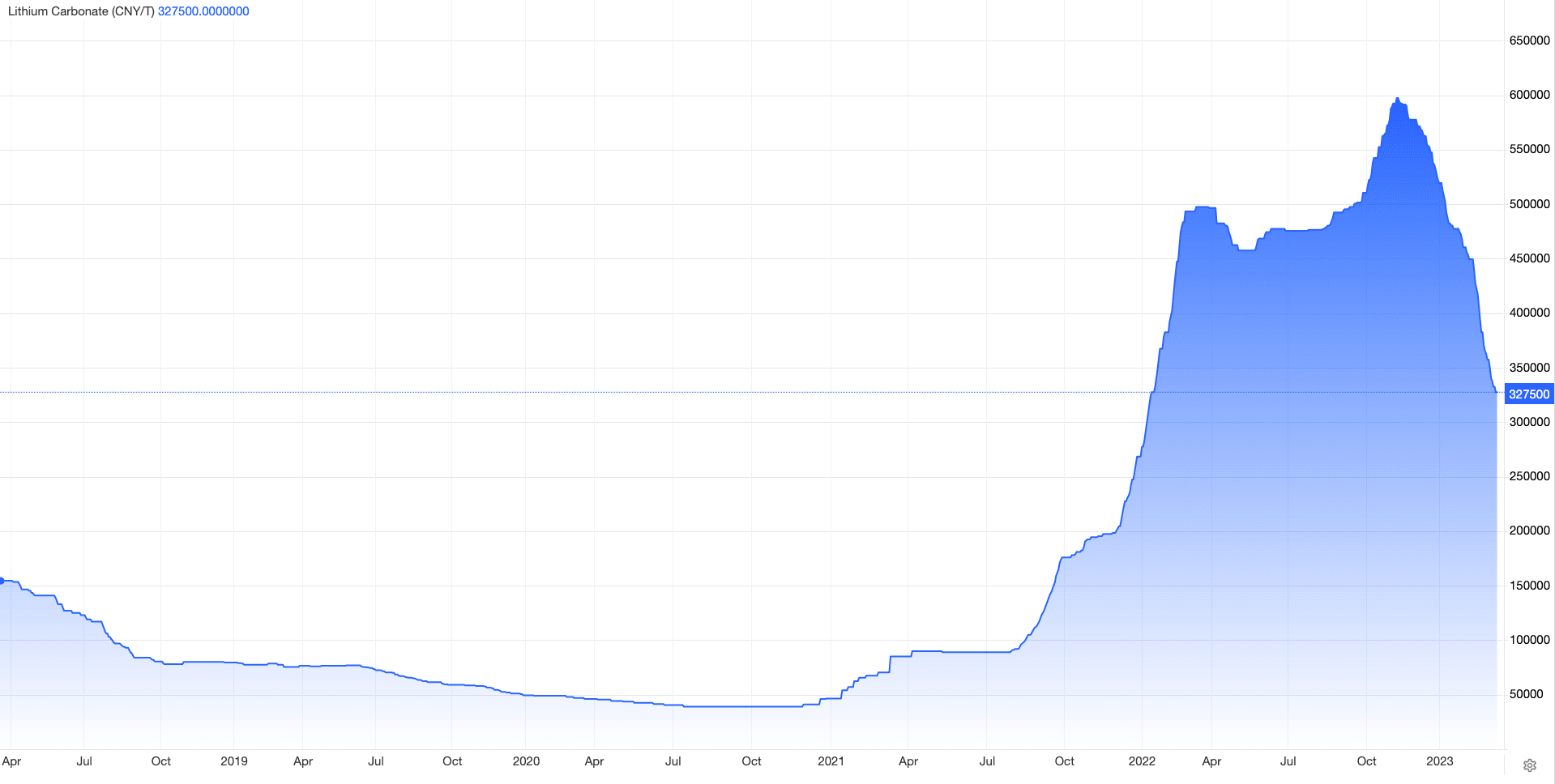

So, why are lithium prices down 40% since last November? Back then, the commodity was trading above US$86,100 per tonne, this figure is now US$47,417, according to Trading View.

The prices of lithium spodumene – the most widely exploited mineral source of lithium – have risen from US$400 a tonne three years ago to a peak of around US$6,000, before pulling back to US$4,500.

Falling EV sales in China, combined with the Lunar New Year holiday, have driven the correction in lithium prices, as Goldman Sachs analyst Aditi Rai told Barron's last month.

Five-year lithium spodumene price

Lithium price (Chinese Yuan). Source: Trading Economics

“Chinese lithium prices took the staircase up but the elevator down,” wrote my Market Index colleague Kerry Sun recently in an article about battery metal stocks, referencing the work of investment bank Citi.

China is one of the world’s largest producers of lithium, alongside Australia, and Chile.

Australian production comprises around 50% of the world’s total lithium output. Allkem (ASX: AKE) and Pilbara Minerals (ASX: PLS) are among the best-known large-cap stocks on the ASX. Allkem’s share price has fallen 7.65% in 2023 so far, while Pilbara shares are down 4.67% in the same period.

But there are many others producing lithium and other metals that are key to the manufacture of EV batteries. Two ASX juniors in the space are Core Lithium (ASX: CXO) and Liontown Resources (ASX: LTR).

Both missed consensus earnings expectations in the first half of FY2023, as we discussed recently with David Franklyn, who heads up the Argonaut Natural Resources Fund. He sums up their results like this:

CXO – “Wait and watch as Core enters the higher-risk commissioning phase.”

LTR – “Significant uplift in construction costs but on track for first production mid-2024.”Why are investors now cautious on lithium?

In a word, 'price'. Franklyn notes (as pointed out above) lithium prices are down 46% in the past six months and 14% in the last week alone.

“This seems appropriate, given the weakening in the lithium price combined with more company-specific issues such as the total overhaul of its management team in the last year,” he says of CXO.

The company has replaced its managing director, chief operating officer and chief financial officer in this timeframe. It is also entering the higher-risk commissioning phase of its Finnis lithium mine in the Northern Territory.

“It also failed to conclude an offtake agreement with Tesla and operations have been negatively impacted by above-average rainfall,” Franklyn says.

And on LTR, he says the market was encouraged by management’s renewed commitment to producing its first lithium by mid-2024,

“But investors are wary of the weakening lithium price, and a capex funding gap of around $200 million due to the higher development cost and mine plan modifications,” Franklyn says.

“Like Core, it’s all about project delivery from here.”

He points out that LTR’s share price is down 15% over the past six months and 12% in a single week.

What are the recent surprises from CXO and LTR?

For CXO, it was the first shipment of 15,000 tonnes of direct shipping ore (DSO) to China just after the end of the half. (Note: This isn’t the main game of spodumene concentrate, which is set to see first production in the first half of calendar 2023).

Franklyn also cites the positive results of the company’s drilling program, with further scope to expand this beyond the initial target of 250,000 tonnes per annum.

Project funding shortfall

The first stage of LTR’s Kathleen Valley mine in Perth, Western Australia is expected to produce up to 550,000 tonnes of spodumene. This figure is set to lift to 770,000 tonnes in stage two.

“Major uncertainty is around development cost and how this will be funded,” says Franklyn.

“Available debt and equity capacity is currently $685 million, which is likely to see it short by around $200 million. Alternatives to close this gap include selling DSO, offtake prepayments, or increasing debt or equity.”

Buy, Hold or Sell?

Rating: Hold (for both)

Franklyn and his team currently rate Core Lithium and Liontown as HOLD. In the former, he notes the company retains about $125 million in cash and is closely watching the progress of its increased production of spodumene before reassessing this view.

It’s a similar story for Liontown: “We’ll watch for project progress and are also looking for clarity around additional funding.”

Outlook: “It’s time to deliver”

Emphasising his earlier remarks, Franklyn says it’s all about project delivery for both LTR and CXO.

In CXO’s case, he believes a re-rating would be in order if it can successfully commission the project on time, within the budget, and hit production targets.

At LTR, Franklyn is watching for more clarity about the effect of mine plan amendments and how management intends to close the capex funding gap – the latter point being critical.

Where are lithium prices headed?

“We expect further weakness in the spodumene price in the medium term, as it pulls back from extraordinarily high levels achieved in 2022,” Franklyn says.

“While this will no doubt have a negative impact on market sentiment towards the sector, the price is still very attractive and will deliver strong returns to scale producers.”

Where are the lithium bulls now?

The commodity price has dipped 40% since last November but Argonaut's David Franklyn isn't dumping ASX lithium stocks just yet.www.livewiremarkets.com

I'm looking to really reduce my LTR position, I have question marks over the whole market broadly and own way too much plus I now want to buy a house back in Perth in 1-3 years. Easy money already been made plus all sorts of things can go wrong when companies actually start mining, the capital cost blowout to build the thing recently was absolutely massive. The company and people like brokers will point to the increased plant capacity and throughput but even my brother laughed and said "Mate, that's the oldest trick in the book." to try and sugarcoat it.It's a long position for me so I am not bothered. Set and forget really.

The whole market is all over the place.

)AVZ would be some peoples best performer the last few monthsLi on my watchlist today

LTR 8.2%

WR1 3.7%

PLS 1.8%

CXO 1.8%

AKE 1.5%

AVZ 0% (lol

I don't know the company or the man but I'd be very, very careful about quickly jumping in on anything when someone suddenly bails like that.Dr T has left RAC. Did not see that coming

Edit: 10% hit on the SP. Tempted to buy a few more. If the drug works and he hasnt/isnt selling out then it should be little impact to a transaction assuming competent people replace and stay

He was ED and CSO of a cancer drug co. Alot of work has been done proving up the efficacy and safety of the drug and hes the #1 SH.I don't know the company or the man but I'd be very, very careful about quickly jumping in on anything when someone suddenly bails like that.

Again I don't know the company at all but when he holds 16M shares they are pretty tokenistic buys perhaps only made as an attempt to soften the blow of him leaving? He says he's not selling now but what about later on when it's not public anymore?He was ED and CSO of a cancer drug co. Alot of work has been done proving up the efficacy and safety of the drug and hes the #1 SH.

The trouble is they found this drug had a few other use cases and went down the path investigating those more than Dr T wanted (it seems) and hes left. Hes stated hes keeping his shares and hes on the board of a microcap so maybe he thinks hes done what he can, onto a new challenge. Who knows but doesnt change the drug, especially if hes keeping his shares his initial belief is still intact. He bought on market 2-3 weeks ago...

Yeah fair points for sureAgain I don't know the company at all but when he holds 16M shares they are pretty tokenistic buys perhaps only made as an attempt to soften the blow of him leaving? He says he's not selling now but what about later on when it's not public anymore?

Liontown

Jesus

Lithium is not gonna be a long term.Lithium shares on an upward correction today as it seems value buyers have jumped in.

LTR rejected a takeover bid and has gone nuts off the back of that.

Lithium is not gonna be a long term.

Turnover money at best

Some other lithium stocks have bounced from this as well. CXO up 19%.Lithium shares on an upward correction today as it seems value buyers have jumped in.

LTR rejected a takeover bid and has gone nuts off the back of that.

Some other lithium stocks have bounced from this as well. CXO up 19%.

Lithium shares on an upward correction today as it seems value buyers have jumped in.

LTR rejected a takeover bid and has gone nuts off the back of that.

Liontown

Jesus

Lithium stocks surge as Liontown rejects a $5.5bn Albemarle takeover bid

Liontown (ASX: LTR) management is going all-in on their belief in the company, rejecting a $2.50 per share takeover bid from global heavyweight Albemarle. The $5.5 billion offer represents a 64% premium to the stock’s last close of $1.53 on Monday.

This comes at a time where lithium valuations are struggling amid a sharp pullback in spot prices. Lithium carbonate prices in China have tumbled below 270,000 yuan a tonne, the lowest in 15 months and down more than 50% since November 2022 highs.

Tuesday’s price action

Liontown shares rallied 31% as the market opened to $2.00 and quickly rallied towards the offer price, reaching session highs of $2.42 in early trade.

The takeover bid inspired a broad-based rally for lithium stocks and by 11:00 am AEDT:

Most of these lithium stocks have been selling off since February and Tuesday’s sharp re-rate has helped many of these names return to positive year-to-date territory.

- Core Lithium (ASX: CXO) +19.2%

- Argosy (ASX: AGY) +15.5%

- Pilbara Minerals (ASX: PLS) +14.8%

- Sayona Mining (ASX: SYA) +13.5%

- Global Lithium (ASX: GL1) +13.0%

- Allkem (ASX: AKE) +12.1%

- Lake Resources (ASX: LKE) +12.0%

- Winsome Resources (ASX: WR1) +11.0%

- Leo Lithium (ASX: LLL) +10.2%

A potential short squeeze

It’s worth noting that short interest among lithium stocks has been aggressively rising since November last year.

Several lithium names have topped the short interest leaderboards. As of Tuesday 28 March, this included (short rank and short % interest):

- (2) Core Lithium 10.04%

- (4) Liontown Resources 8.91%

- (6) Sayona Mining 8.61%

- (13) Vulcan Energy 6.67%

- (18) Lake Resources 6.34%

Selloff opens the door for M&A

The lithium selloff has put the industry in a rather awkward place as it tries to balance the current weakness in Chinese EV sales and spot prices against long-term EV demand forecasts and the strategic nature of the battery metal.

Before Tuesday’s re-rate, most ASX-listed lithium stocks were down 20-30% year-to-date which has now prompted one of the world’s largest lithium companies – Albemarle – to try and stock up on a high-quality project at discounted price.

To add some perspective, Liontown expects its Kathleen Valley Lithium Project to hit production status in the second quarter of 2024. The project boasts a ‘globally significant’ Mineral Resource Estimate of 156 million tonnes at grades of 1.4%.

A November 2021 Definitive Feasibility Study said the project is expected to supply approximately 5% of global spodumene, ramping up to around 6% by 2029. The project was stated to have a post-tax NPV of $4.2 billion, based on a mine life of 23 years and referenced a long-term weighted spodumene price of US$1,382 a tonne.

Interesting, Pilbara Minerals received an average realised price of US$4,993 a tonne for its spodumene in the first half of FY23. Even if prices were to halve from those levels – it's still well-above the DFS’ reference price.

Not the first time

This isn’t the first time Albemarle has had a crack at buying Liontown.

The company received non-binding indicative proposals from Albemarle at $2.35 on 3 March 2023 and $2.20 per share on 20 October 2022.

There are three interesting takeaways from this:

- The 3 March takeover offer was not announced to the market. But Liontown shares rallied 13% to $1.63 on that day

- The new $2.50 takeover represents a 13.6% increase compared to the October bid

- Between 20 October 2022 and 27 March 2023 (the day before the new offer) – Liontown shares have tanked around 17%

Why Liontown rejected the offer

The Liontown Board noted the “opportunistic timing of Albemarle’s Indicative Proposal, coinciding with recent softness in companies exposed to the lithium sector and the pre-production status of the Kathleen Valley Project.”

In other words: Why are you trying to lowball us?

The announcement also pointed out five key points including:

Value aside, Kathleen Valley faces a substantial funding shortfall after a January update flagged that capital costs to first production jumped to $895 million from $473 million.

- A significant amount of de-risking has occurred for Kathleen Valley in recent months

- There are extensive growth options for the project including Director Shipping Ore

- There are few projects that have the scale, quality and mine life as Kathleen Valley

- The near-and-long term looks positive for lithium

- Albemarle has several other benefits from acquiring Kathleen Valley, including significant synergies from its existing operations in Australia

Management said the company “continues to progress a number of attractive funding options for the remaining capital at the Kathleen Valley Lithium Project and expects to update the market on this front in the near term.”

All the experts were suggesting that this would be the case, however it seems like the $100/barrel expectation has stalled a little bit.I've recently loaded up a on energy stocks.

If oil could hit $100/barrel that'd be great.