cartwright

Brownlow Medallist

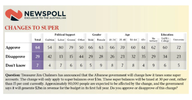

Some numbers:

At age 25, he says you would have to be earning $200,000 a year, to have $3 million in super by age 67 (under the assumption your super contributions are 12 per cent per year, earnings were 5 per cent per year for the next 42 years and you pay 1 per cent in fees).

And

Long story short, to hit the $3m cap, you either have to start by earning four-times the typical salary and keep earning at that rate for the next 42 years, or you'd need to earn double the long-term average investment performance each and every year for 42 years," he explained.

So yeah, think the average person doesn’t need to worry about this.

At age 25, he says you would have to be earning $200,000 a year, to have $3 million in super by age 67 (under the assumption your super contributions are 12 per cent per year, earnings were 5 per cent per year for the next 42 years and you pay 1 per cent in fees).

And

Long story short, to hit the $3m cap, you either have to start by earning four-times the typical salary and keep earning at that rate for the next 42 years, or you'd need to earn double the long-term average investment performance each and every year for 42 years," he explained.

So yeah, think the average person doesn’t need to worry about this.