rdhopkins2

Carpe Diem

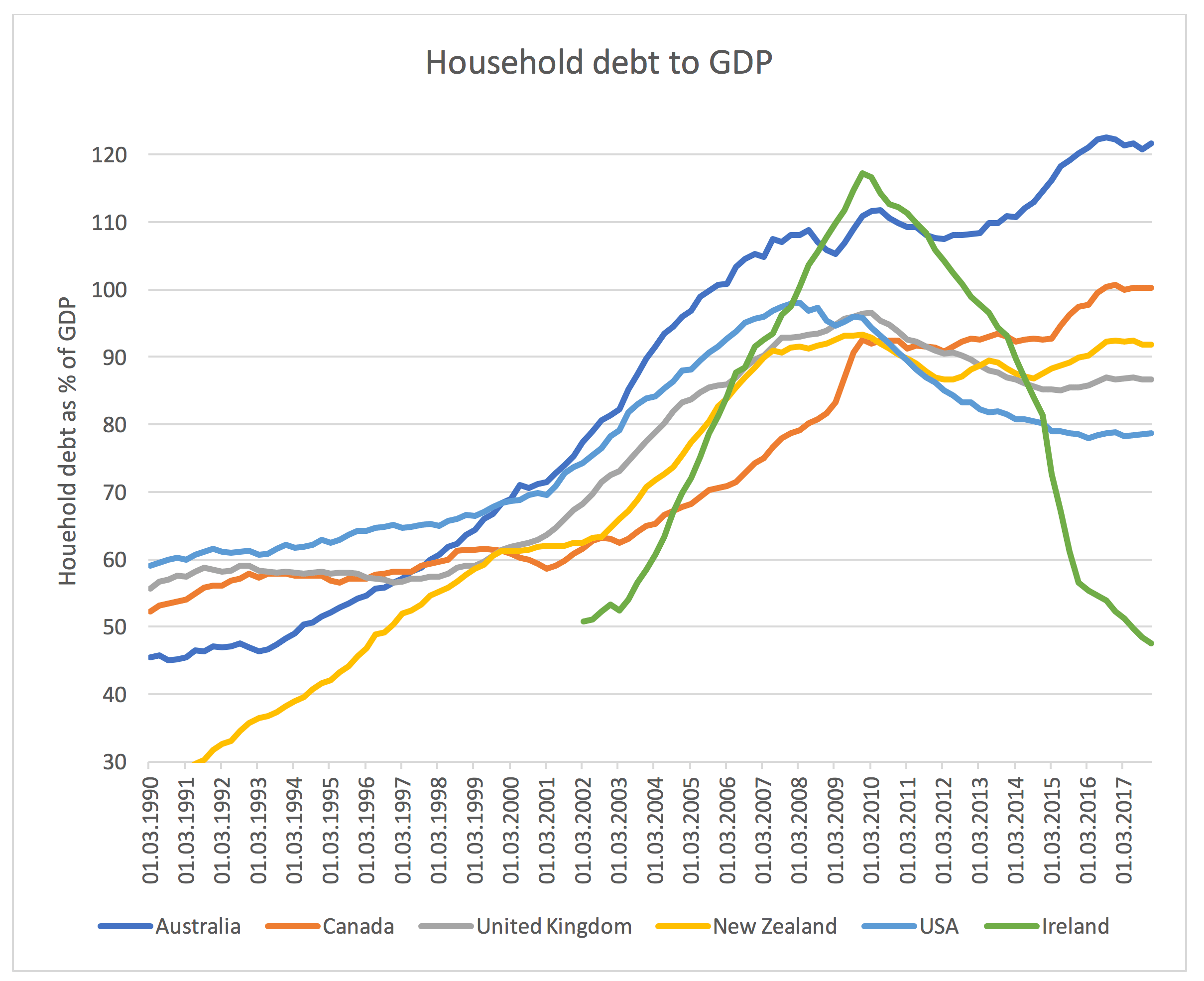

The ability to obtain credit in Australia has seemingly never been easier. The lure of marketers spruiking buy now, pay later sees many Australians fall in to financial traps.

Many big companies have for a long time offered “buy now, pay later,” interest free terms on store cards. We have had credit cards in Australia since the 1970’s. There is now Afterpay, Zippay and I’m sure there are many others out there.

Back in the day, if you couldn’t afford to pay for a product upfront, stores offered lay-bys where you would pay the product off in instalments BEFORE you could take the product home.

Can’t afford a new car? Well that’s okay says the car salesman, we can help with the finance too.

Has Australia become so used to instant gratification that the use of credit is normal, even for small purchases (hey I’ll just whack that on the credit card or an afterpayment method…)

Has Australia become so used to instant gratification that the use of credit for anything is normal?

Does credit in Australia need to be more highly regulated?

Note, this is not intended to discuss mortgages. I’ll make a separate one for that.

Many big companies have for a long time offered “buy now, pay later,” interest free terms on store cards. We have had credit cards in Australia since the 1970’s. There is now Afterpay, Zippay and I’m sure there are many others out there.

Back in the day, if you couldn’t afford to pay for a product upfront, stores offered lay-bys where you would pay the product off in instalments BEFORE you could take the product home.

Can’t afford a new car? Well that’s okay says the car salesman, we can help with the finance too.

Has Australia become so used to instant gratification that the use of credit is normal, even for small purchases (hey I’ll just whack that on the credit card or an afterpayment method…)

Has Australia become so used to instant gratification that the use of credit for anything is normal?

Does credit in Australia need to be more highly regulated?

Note, this is not intended to discuss mortgages. I’ll make a separate one for that.